Market Overview and Regional Positioning

The global black mass recycling market exhibits distinct regional growth trajectories, with Europe and North America providing strong regulatory support and emerging as high-margin segments despite Asia-Pacific’s current dominance.

Market Distribution (2025)

Europe represents approximately USD 1.2–1.5 billion, or 20–26% of global black mass recycling volumes, with projected annual growth of 20% through 2035. North America accounts for USD 1.0 billion, representing roughly 17% of the global market. Asia-Pacific maintains market dominance, commanding 50–60% of global volumes, primarily through China, South Korea, and Japan, which possess established recycling infrastructure and high electric vehicle penetration.

Regulatory Drivers and Capacity Requirements

- European Union: Demand-Pull Framework

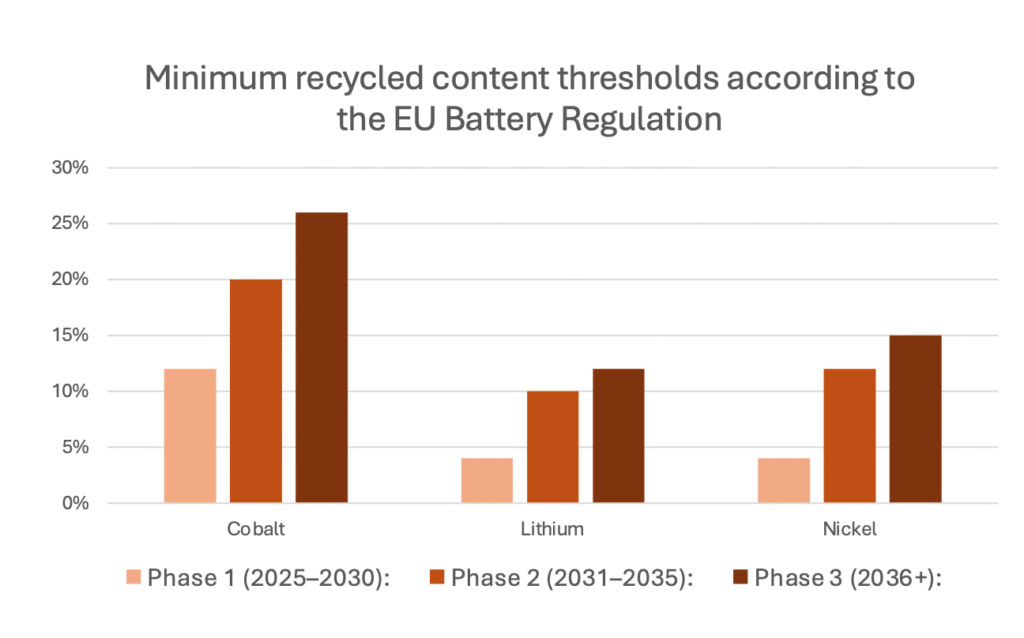

The EU Battery Regulation 2023/1542, implemented in 2024, fundamentally restructures recycling economics through mandatory minimum recycled content thresholds

Current EU recycling capacity remains insufficient to meet Phase 1 requirements necessitating urgent investment in hydrometallurgical and pyrometallurgical facilities. The EU will initially depend on imported black mass from Asia to bridge capacity gaps. Phase 2 requirements (2031–2035: 20% cobalt, 10% lithium, 12% nickel) demand substantial capacity scaling—potentially tripling current levels.

This regulatory architecture creates a structural supply shortage that incentivises domestic capacity development and supports premium pricing for compliant recycled materials.

- United States: Supply Chain Localization

The Inflation Reduction Act (IRA) mandates critical mineral content in batteries extracted or processed in the United States or Free Trade Agreement countries increase from 40% (2024) to 80% (2027). US-sourced and processed black mass qualifies as domestically processed material, thereby circumventing China’s dominance in lithium and cobalt refining and directly supporting domestic recyclers.

Example calculation: The economic incentive structure is substantial: recyclers supplying cathode-active materials to a 50 GWh/year battery manufacturing plant can potentially access a $35/kWh manufacturing credit, potentially generating USD 1.75 billion in annual potential downstream value (USD 35/kWh × 50 GWh). This mechanism creates direct pull-through demand for black mass processors and accelerates capacity investment.

- Asia-Pacific: Extended Producer Responsibility Without Recycled Content Mandates

Asian regulatory frameworks differ fundamentally from Western approaches. China implements Extended Producer Responsibility with battery passport-style end-of-life tracking; South Korea mandates that battery producers finance collection and recycling systems; and Japan operates a voluntary industry-led framework. Critically, none of these jurisdictions imposes recycled content mandates, creating a supply-push dynamic distinct from the EU’s demand-pull model.

Chemistry Mix and Operating Margins

Battery chemistry fundamentally determines black mass recycling profitability across regions.

- NMC vs. LFP Economics

NMC (nickel-manganese-cobalt) black mass recovered from vehicles contains high concentrations of valuable cobalt and nickel, yielding approximately USD 7,300–12,800 per ton. LFP (lithium iron phosphate) black mass, which contains no nickel, recovers only USD 1,450–2,965 per ton. Processing costs remain consistent across chemistries at USD 5,000–8,000 per ton, resulting in gross margins of USD 2,000–5,000 per ton for NMC versus breakeven or negative margins for LFP.

- Regional Chemistry Divergence

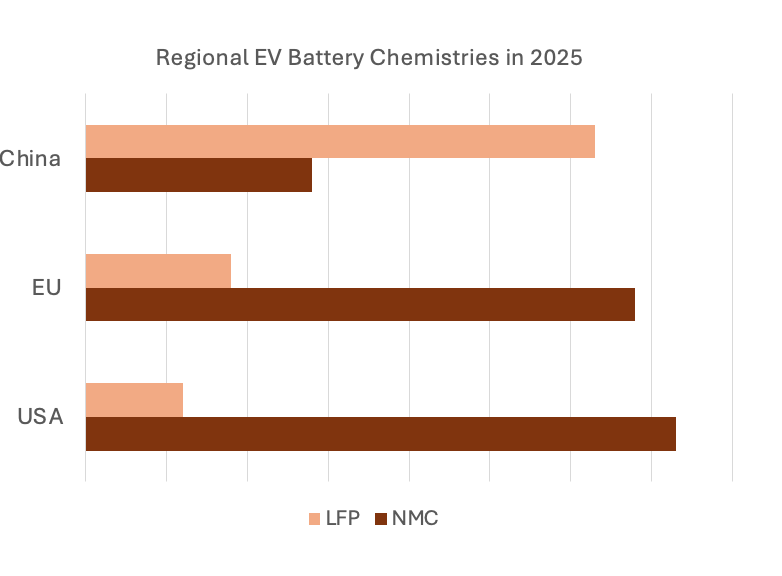

The US and EU electric vehicle markets are dominated by NMC chemistry, whereas China’s market is predominantly LFP. This divergence directly determines regional recycling profitability: Western recyclers benefit from higher-value feedstock, while Asian recyclers process lower-margin chemistries at significantly larger volumes.

Chinese original equipment manufacturers – including BYD, NIO, Li Auto, and SAIC- predominantly use LFP chemistry. Their growing market share in Europe and North America, particularly in price-sensitive segments, represents the critical variable determining future regional profitability dynamics.

Structural Advantages and Margin Implications

- EU Regulatory Advantage

The EU regulatory mandate creates a decisive structural difference: recyclers must process LFP black mass regardless of margin profitability. The 10% lithium recycled content requirement mandates lithium extraction and refinement also from LFP feedstock, generating revenue streams from materials that would otherwise be economically marginal.

This regulatory framework guarantees demand for otherwise uneconomical LFP black mass processing, effectively subsidising recycler margins and enabling profitable operations across chemistry types.

- US Selective Targeting

US recyclers, operating under supply-security rather than recycled-content mandates, retain the flexibility to selectively target higher-margin NMC feedstock while avoiding low-margin LFP processing. This selectivity provides margin optimisation benefits but creates supply-chain rigidity compared to EU competitors with integrated, chemistry-agnostic processing capabilities.

Strategic Implications

Both the USA and the EU provide market opportunities for black mass recyclers, but the impacts are differentiated by regulatory framework:

- Europe: Regulatory certainty and demand guarantee support capacity investment despite near-term supply constraints and margin compression from LFP penetration.

- North America: Strong IRA incentives support profitable NMC-focused operations, with selective LFP processing as Chinese OEM penetration accelerates.